by Richard Cull

August 2022 Market Recap & Commentary

Commentary

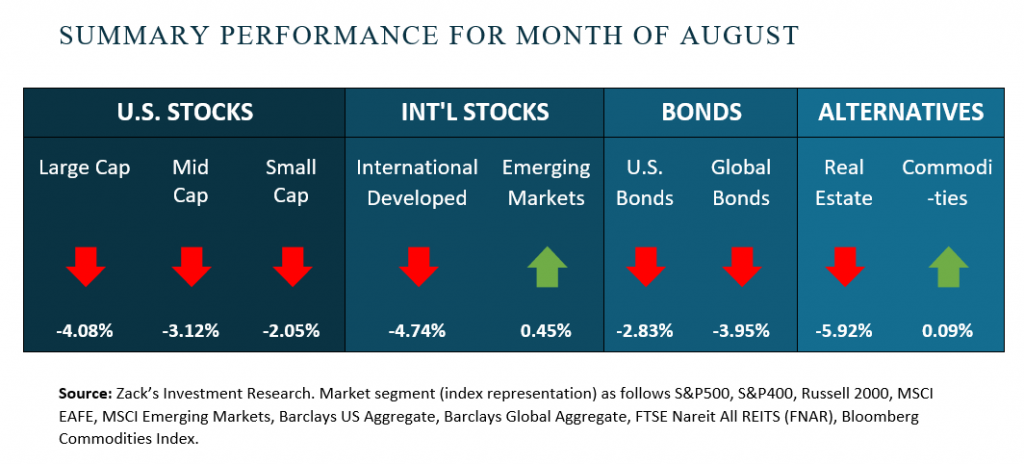

The month of August saw negative numbers across almost all asset classes. These markets are like riding a seesaw but less fun. August marked the seventh straight month the S&P 500’s return was the opposite (negative/ positive) of the preceding month. If that pattern holds, we can look forward to positive returns for September.

This part of the calendar is traditionally one of the slowest for investment news. Coming off corporation’s 2nd quarter earnings releases, volumes slow on the dearth of new information and last hurrah vacations of the summer. This can amplify seemingly insignificant happenings and foster outsized market swings.

Looking back over August, we really had only three pieces of meaningful news. One, the jobs report came in very strong showing over 500,000 new jobs created and the unemployment rate still hovering near all-time lows. Two, the Personal Consumption Expenditures (PCE) {Fed’s preferred gauge of inflation} came in slightly below expectations. Three, Fed Chairman Jerome Powell spoke at the Jackson Hole Symposium.

Elaborating on number three, The US Federal Reserve hosts an annual gathering of economists, central bankers, and policy makers from across the globe to “promote public discussion and exchange ideas.” The Fed Chairman’s speech is always the highlight as investors look for clues about future monetary policy.

Two years ago, Chairman Powell made the case for letting prices rise above the Fed’s 2% inflation target and last year he called this bout of inflation “transitory.” This year he delivered a very direct, somber message catching the markets by surprise. In short, Chairman Powell said the Fed is committed to bringing down inflation and they will most likely require higher rates over a longer time frame. In that eight-minute speech he contradicted the theory behind the markets recent run up…that rate hikes were near a peak and would actually begin falling next year.

Traders reacted immediately taking the major equity benchmarks down over 3% before the closing bell rang and falling further every market day since. This is another pitfall of thinking short-term, one has to anticipate market-moving news (i.e. Market timing)…which is impossible.

As experienced long-term investors, we feel that taming inflation is vital to consumer spending and thus corporate profitability and thus investment returns. The Federal Reserve is a major cause of this inflation as a result of their much-longer-than-needed easy-money policies during COVID. Their current rhetoric and tightening policies along with the easing of supply bottlenecks and end of economic shut-downs should prove healthy for the markets in the long run.

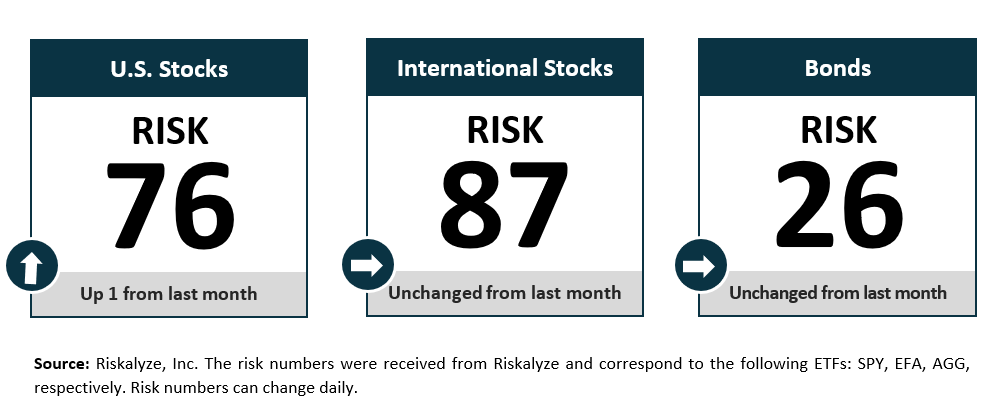

Risk Numbers

The Risk Number is at the heart of a sophisticated set of tools to precisely measure the appetite and capacity for risk that each client has, and demonstrate their alignment with the portfolios built for them. The following graphic shows the risk of various asset classes as measured on a scale of 1-99 (1 being the most conservative and 99 being the most aggressive) as of the date above.

Centric's Approach

We start with a Risk Number, a measurable way to pinpoint how much risk you want, need, and already have. Then, your wealth advisor will optimally allocate our investments to help you reach your financial goals. Along the way, you will receive transparency of information, seamless proactive service and the trust and accountability you need to stay on track. All of this will lead to your personal comprehensive investment strategy that is powerful, disciplined, responsive.

Sources:

Centric’s Market Assumption Disclosures: This information is not intended as a recommendation to invest in any particular asset class or strategy or product or as a promise of future performance. Note that these asset class assumptions are passive, and do not consider the impact of active management. All estimates in this document are in US dollar terms unless noted otherwise. Given the complex risk-reward trade-offs involved, we advise clients to rely on their own judgment as well as quantitative optimization approaches in setting strategic allocations to all the asset classes and strategies. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Assumptions, opinions and estimates are provided for illustrative purposes only. They should not be relied upon as recommendations to buy or sell securities. Forecasts of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. If the reader chooses to rely on the information, it is at its own risk. This material has been prepared for information purposes only and is not intended to provide, and should not be relied on for, accounting, legal, or tax advice. The outputs of the assumptions are provided for illustration purposes only and are subject to significant limitations. “Expected” return estimates are subject to uncertainty and error. Expected returns for each asset class can be conditional on economic scenarios; in the event a particular scenario comes to pass, actual returns could be significantly higher or lower than forecasted. Because of the inherent limitations of all models, potential investors should not rely exclusively on the model when making an investment decision. The model cannot account for the impact that economic, market, and other factors may have on the implementation and ongoing management of an actual investment portfolio. Unlike actual portfolio outcomes, the model outcomes do not reflect actual trading, liquidity constraints, fees, expenses, taxes and other factors that could impact future returns. Asset allocation/diversification does not guarantee investment returns and does not eliminate the risk of loss.

Index Disclosures: Index returns are for illustrative purposes only and do not represent any actual fund performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

Riskalyze Disclosure: The Risk Number® is a proprietary scaled index developed by Riskalyze to reflect risk for both advisors and their clients. The Risk Number is at the heart of a sophisticated set of tools to precisely measure the appetite and capacity for risk that each client has, and demonstrate their alignment with the portfolios built for them.

Shaped like a speed limit sign, the Risk Number gives advisors and investors a common language to use when setting expectations, recognizing risk and making portfolio selections. Just like driving faster increases hazards, a higher Risk Number equates with higher levels of risk.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

Get in Touch

Ready to take control of your finances and enjoy more of what matters in your life?