by Richard Cull

April 2022 Market Recap & Commentary

Commentary

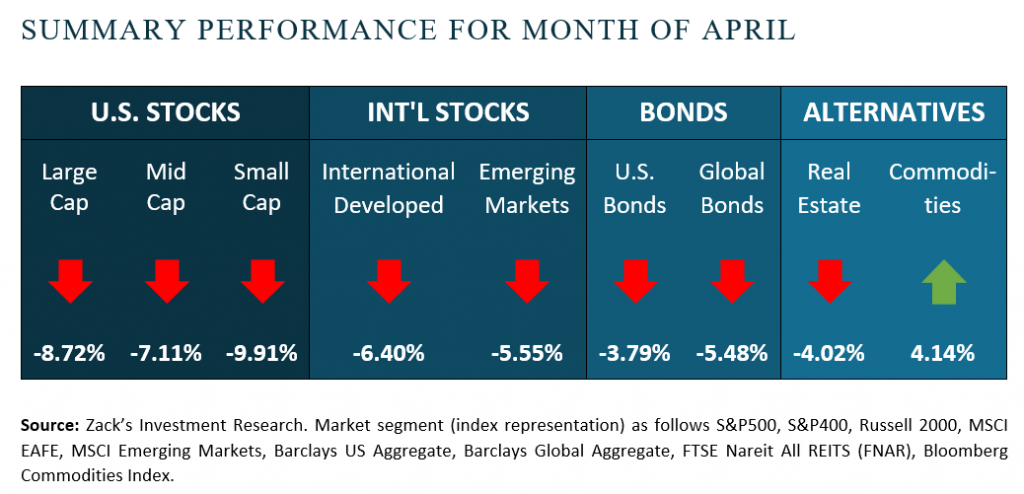

The month of April continued the 2022 theme of increased volatility and Bulls vs. Bears tug of war. Almost every asset class was down meaningfully for the month with the tech heavy NASDAQ now officially in Bear market territory year-to-date (down more than 20%).

Headlines often drive the day-to-day movements of investments over the short-term and our always-on news cycle ensure there are plenty to attract eyeballs. When we weed out the lesser stories (which we refer to as “noise”), the very impactful situations of high inflation, a tightening Federal Reserve and continuing war in Ukraine (Big Three) command investors’ attention. The gravity of these situations combined with the uncertainty of their resolutions definitely warrants the level of volatility we are experiencing.

Issues such as corporate profitability, consumer demand, energy prices, supply chains, labor conditions, etc. are receiving far less attention than the aforementioned Big Three. In the long-term however, these issues are fundamental to analysis and determining security prices. Since the first of the year these issues have been giving off mixed signals.

These mixed signals are adding to volatility and fuel the Bulls vs. Bears tug of war. Bulls are a term used for investors who think the market will rise. The Bull case currently points to growing corporate profits, increasing profit margins, strong consumer demand and historically low unemployment. Bears are the opposite, referring to investors expecting the market to fall. The Bear case points to a tightening Fed, high oil prices, supply chain restrictions, high inflation, and rising interest rates.

Always present, the tug of war really heats up with the reporting of economic/ investment news such as the monthly employment report, Federal Reserve Governors reporting to Congress or even when Tesla’s discloses its latest quarterly car production. Many days / weeks / months this year have seen Bears take control…the month of April being the most recent example.

2022 has provided both Bulls & Bears with plenty of material to justify their views. It seems that the number and severity of today’s issues will continue to foster this environment of uncertainty with a possibility of overreaction to the downside (fear). Experience has taught us to be mindful of emotions and remain strategic with the portfolios entrusted to us even during tough times such as these. The Bears may be in control for a while but at Centric we know that Bulls prevail in the long-term!

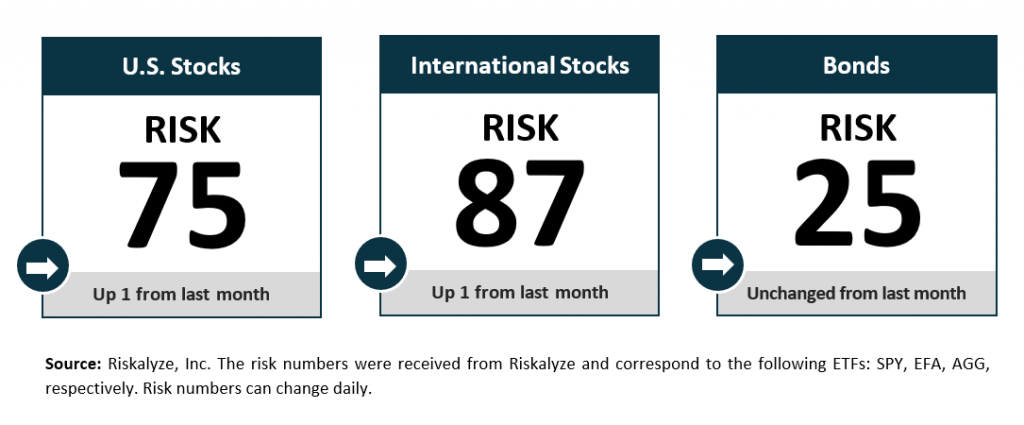

Risk Numbers

The Risk Number is at the heart of a sophisticated set of tools to precisely measure the appetite and capacity for risk that each client has, and demonstrate their alignment with the portfolios built for them. The following graphic shows the risk of various asset classes as measured on a scale of 1-99 (1 being the most conservative and 99 being the most aggressive) as of the date above.

Centric's Approach

We start with a Risk Number, a measurable way to pinpoint how much risk you want, need, and already have. Then, your wealth advisor will optimally allocate our investments to help you reach your financial goals. Along the way, you will receive transparency of information, seamless proactive service and the trust and accountability you need to stay on track. All of this will lead to your personal comprehensive investment strategy that is powerful, disciplined, responsive.

Sources:

Centric’s Market Assumption Disclosures: This information is not intended as a recommendation to invest in any particular asset class or strategy or product or as a promise of future performance. Note that these asset class assumptions are passive, and do not consider the impact of active management. All estimates in this document are in US dollar terms unless noted otherwise. Given the complex risk-reward trade-offs involved, we advise clients to rely on their own judgment as well as quantitative optimization approaches in setting strategic allocations to all the asset classes and strategies. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Assumptions, opinions and estimates are provided for illustrative purposes only. They should not be relied upon as recommendations to buy or sell securities. Forecasts of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. If the reader chooses to rely on the information, it is at its own risk. This material has been prepared for information purposes only and is not intended to provide, and should not be relied on for, accounting, legal, or tax advice. The outputs of the assumptions are provided for illustration purposes only and are subject to significant limitations. “Expected” return estimates are subject to uncertainty and error. Expected returns for each asset class can be conditional on economic scenarios; in the event a particular scenario comes to pass, actual returns could be significantly higher or lower than forecasted. Because of the inherent limitations of all models, potential investors should not rely exclusively on the model when making an investment decision. The model cannot account for the impact that economic, market, and other factors may have on the implementation and ongoing management of an actual investment portfolio. Unlike actual portfolio outcomes, the model outcomes do not reflect actual trading, liquidity constraints, fees, expenses, taxes and other factors that could impact future returns. Asset allocation/diversification does not guarantee investment returns and does not eliminate the risk of loss.

Index Disclosures: Index returns are for illustrative purposes only and do not represent any actual fund performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

Riskalyze Disclosure: The Risk Number® is a proprietary scaled index developed by Riskalyze to reflect risk for both advisors and their clients. The Risk Number is at the heart of a sophisticated set of tools to precisely measure the appetite and capacity for risk that each client has, and demonstrate their alignment with the portfolios built for them.

Shaped like a speed limit sign, the Risk Number gives advisors and investors a common language to use when setting expectations, recognizing risk and making portfolio selections. Just like driving faster increases hazards, a higher Risk Number equates with higher levels of risk.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

Get in Touch

Ready to take control of your finances and enjoy more of what matters in your life?