by Oscar R. Mondragon

How Far Could $1 Million Go in Retirement?

A million dollars used to be the ultimate target for retirement portfolios. Retiring as a millionaire brought status and confidence that you could live comfortably during your golden years.

If you retired with $1 million in 1970, you probably didn’t have to worry about your nest egg running out, even with a lavish lifestyle. I would be like retiring with $6.9 million today. 1

Retire with $1 Million in the ‘80s, and it would have been like retiring with $3.35 million in 2021. 1

And in 1990?

A cool $1 million would have gone twice as far as it does these days.

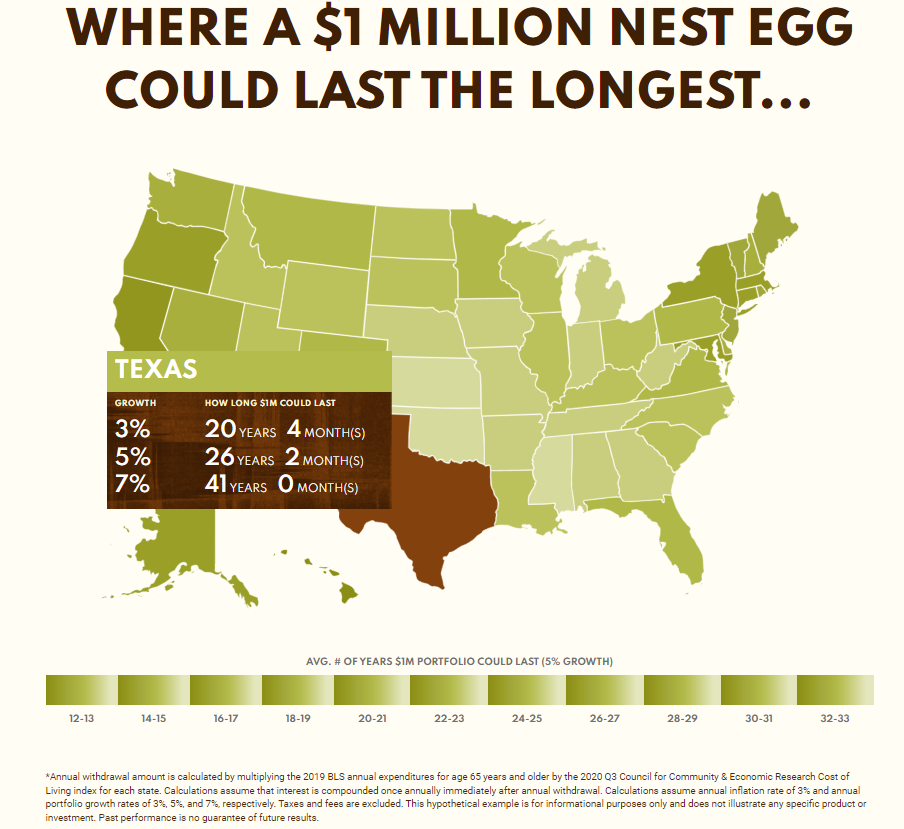

Clearly, $1 million doesn’t go as far as it used to. Just how far could it go these days? The answer depends on how and where you live. In retirement, as in real estate, location is everything (or, at least, it’s a lot).

What's missing from this picture?

The estimates in the map above cover the basics and paint a potentially realistic picture. They don’t fill in every piece of the puzzle, though. In fact, some key aspects of life in retirement are hypothetical scenarios shown in our $1 million retirement map. Here are a few of them.

Higher than Average Expenses

The averages used to calculate expenses in retirement may not fit how you actually live. If you’re spending more or less than the average for your area, your expenses could drain your savings faster or make them last longer. That’s’ why you can’t fully rely on averages to anticipate how long a nest egg can last.

The Fun Stuff!

Retirement isn’t just about covering the basics to get by. You retired because you want to enjoy your time and do fun things, maybe even things you had put off while working or raising a family. Whatever that fun looks like go you, our estimates don’t capture these costs.

Performance Realities

Our calculations assumed stable annual growth for retirement portfolios. Of course, that’s not realistic or reliable. Investment performance can vary drastically from year to year. A personal retirement income plan should account for these types of ups and downs. It should also build in some flexibility for responding to performance changes while keeping you on track to hit your goals.

What will cost you the most in retirement?

Health Care

Health care is a significant expense for most retirees. In fact, a healthy couple retiring at age 65 in 2021 could need $662,156 or more to cover their health care costs for the rest of their lives. Perhaps ironically, those of us fortunate enough to retire in good health could end up paying more in health care costs than retirees with health problems. Why? Because, when we live longer, we’ll be paying for health care costs longer.

Long-Term Care

About 70% if retirees who are age 65 or older will need long-term care at some point in their lives. These costs vary by location and length of stay. Still, nearly 50% if retirees will need about a year of long-term care. Depending on where you live and whether you have LTC coverage, that could run anywhere from $54,000 to more than $105,000 in out -of-pocket costs every year. And those costs are only getting more expensive. By 2030, expect those costs to be at least 35% higher.

Taxes

Many folks are surprised by the taxes they owe after they stop working. Tax laws are ever-changing and can have a significant impact on how much you owe in taxes during retirement. Fortunately, proactive planning may help mitigate the impact of taxes on your expenses.

Lifestyle

What do you want to do in retirement? What kind of extras do you want to enjoy and share with your loved ones? What does your dream lifestyle in retirement look like? The price tag associated with those dreams is a big variable in your personal retirement calculations.

Surprised by what you learned? Everyone’s retirement journey looks different, and the averages leave out a lot of detail.

The Million Dollar Question:

How Do YOU want to live in Retirement?

A cool million just doesn’t go as far as it used to. Were you shocked by how little $1 million could last in some places? Or how long in others? It certainly illustrates what a difference cost of living can make to your finances.

And it also shows that averages leave out a lot of important detail.

While benchmarking your likely expenses is a good starting point, tweaking them for your personal situation is critical. As is remembering that your expenses will change as you journey through retirement. In my experience, folks typically spend more on lifestyle, family, and fun at the beginning of their retirement and may see their medical and long-term care expenses increase as they age.

Bottom line? For financial life management and personal advice, consider contacting Centric to help you prepare for the retirement years ahead of you! We’ll navigate them together.

SOURCES

1 - https://www.bls.gov/data/inflation_calculator.htm

2 – https://www.cnbc.com/2019/07/18/retiring-this-year-how-much-youll-need-for-health-care-costs.html

3 – https://www.hhs.gov/aging/long-term-care/index.html

4 – https://www.genworth.com/aging-and-you/finances/cost-of-care.html

Investing involves risk including the potential loss of principal. No investment strategy can guarantee a profit or protect against loss in periods of declining values. Past performance does not guarantee future results.

Get in Touch

Ready to take control of your finances and enjoy more of what matters in your life?