by Richard Cull

Year End 2021 Market Recap & Commentary

“Always invest for the long term.”

Warren Buffet

The Year on Main Street

Measured against the tumultuous events that started in February 2020, the 2021 calendar year was very subdued on “Main Street.”

The first two months had a few notable occurrences including the storming of the Capitol, the inauguration of President Biden, the second impeachment of President Trump, and a severe widespread winter storm unofficially referred to as “snowmageddon.”

The rest of the year revolved around COVID… from the vaccine to the Delta variant, to the booster, and now the Omicron variant.

In the face of these issues, Americans adapted and moved forward in what can be labeled the “Great Reopening.”

The Year on Wall Street

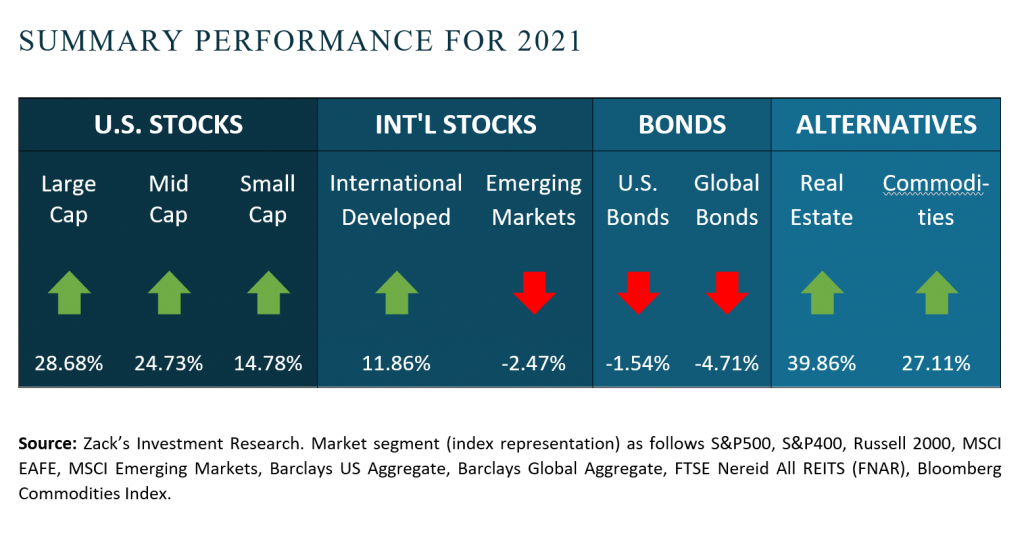

Continuing the run that began at the bottom of the pandemic sell off (March 23, 2020), equities move steadily higher throughout the year. Volatility was subdued and the S&P 500 registered a streak of seven consecutive months with positive returns at one point.

The headline grabbing return of the S&P 500 however, overshadows the very uneven returns of the other equity benchmarks. Smaller U.S. stocks and developed international stocks were solid but did not keep up with U.S. Mega-cap biased S&P 500 index. Emerging markets, dragged down by China, and Gold actually had negative returns for the year.

The other major asset class, fixed income, experienced a down year as rates moved higher with inflation. With seemingly little regard for the increase in risk, investors sold bonds and chased the aforementioned stock market.

The Year Ahead

That is the past.

At present, the economy is very strong with robust consumer demand, strong corporate balance sheets, expanding corporate earnings and historically low interest rates.

The future, however, is what's paramount to the markets. It is apparent to us that the upward momentum in the economy will continue, barring some unforeseen event (natural disaster, war, terrorism, etc). The ending levels of the markets in 2022 will depend on how investors deal with a new set of challenges.

As always there is a list of uncertainties. Experience has taught us most of these are short term in nature and make great CNBC headlines but ultimately will not disrupt the economy.

The real challenges for the markets that must be worked through include persistent inflation, the end of the fed's “easy money” policy and a return to lower, albeit normal rates of earnings growth.

We foresee a tug-of-war between these big three and the solid underlying market fundamentals. This will most likely go back and forth all year, resulting in higher volatility and perhaps a couple of tense weeks. Remember, market declines are fairly common with 5% pullbacks occurring on average three times a year and 10% drawdowns occurring every 19 months.

Centric's Approach

At Centric, we are LONG-TERM, FUNDAMENTAL investors.

We speak and write that whenever possible. Our task is to grow our clients’ assets by building diversified portfolios tailored for their individual goals and within their individual parameters. To those ends we believe investing is a discipline built on a process developed through education, analysis and experience.

The theme of last year’s letter was the quote, “a believer in a better tomorrow” by Benjamin Graham who is widely considered the father of value investing. This year we feel the most relevant quote comes from his famous student, Warren Buffet …simply and concisely, “Always invest for the long term.”

Sources:

Centric’s Market Assumption Disclosures: This information is not intended as a recommendation to invest in any particular asset class or strategy or product or as a promise of future performance. Note that these asset class assumptions are passive, and do not consider the impact of active management. All estimates in this document are in US dollar terms unless noted otherwise. Given the complex risk-reward trade-offs involved, we advise clients to rely on their own judgment as well as quantitative optimization approaches in setting strategic allocations to all the asset classes and strategies. References to future returns are not promises or even estimates of actual returns a client portfolio may achieve. Assumptions, opinions and estimates are provided for illustrative purposes only. They should not be relied upon as recommendations to buy or sell securities. Forecasts of financial market trends that are based on current market conditions constitute our judgment and are subject to change without notice. We believe the information provided here is reliable, but do not warrant its accuracy or completeness. If the reader chooses to rely on the information, it is at its own risk. This material has been prepared for information purposes only and is not intended to provide, and should not be relied on for, accounting, legal, or tax advice. The outputs of the assumptions are provided for illustration purposes only and are subject to significant limitations. “Expected” return estimates are subject to uncertainty and error. Expected returns for each asset class can be conditional on economic scenarios; in the event a particular scenario comes to pass, actual returns could be significantly higher or lower than forecasted. Because of the inherent limitations of all models, potential investors should not rely exclusively on the model when making an investment decision. The model cannot account for the impact that economic, market, and other factors may have on the implementation and ongoing management of an actual investment portfolio. Unlike actual portfolio outcomes, the model outcomes do not reflect actual trading, liquidity constraints, fees, expenses, taxes and other factors that could impact future returns. Asset allocation/diversification does not guarantee investment returns and does not eliminate the risk of loss.

Index Disclosures: Index returns are for illustrative purposes only and do not represent any actual fund performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indices are unmanaged and one cannot invest directly in an index.

Riskalyze Disclosure: The Risk Number® is a proprietary scaled index developed by Riskalyze to reflect risk for both advisors and their clients. The Risk Number is at the heart of a sophisticated set of tools to precisely measure the appetite and capacity for risk that each client has, and demonstrate their alignment with the portfolios built for them.

Shaped like a speed limit sign, the Risk Number gives advisors and investors a common language to use when setting expectations, recognizing risk and making portfolio selections. Just like driving faster increases hazards, a higher Risk Number equates with higher levels of risk.

General disclosure: This material is intended for information purposes only, and does not constitute investment advice, a recommendation or an offer or solicitation to purchase or sell any securities to any person in any jurisdiction in which an offer, solicitation, purchase or sale would be unlawful under the securities laws of such jurisdiction. Reliance upon information in this material is at the sole discretion of the reader. Investing involves risks.

Get in Touch

Ready to take control of your finances and enjoy more of what matters in your life?